Connecting the live music industry

Report: Who Owns Europe’s Festivals and Venues?

February10

A newly published set of European ownership maps from the European Mapping Project on Ownership Concentration in Live Music provides an updated overview of who owns and controls key assets across the continent’s live music sector.

While audiences primarily encounter festivals and concerts through programming and live experiences, the ownership structures behind these events play a decisive role in determining who operates stages, how financial risks are allocated, and where revenues ultimately flow.

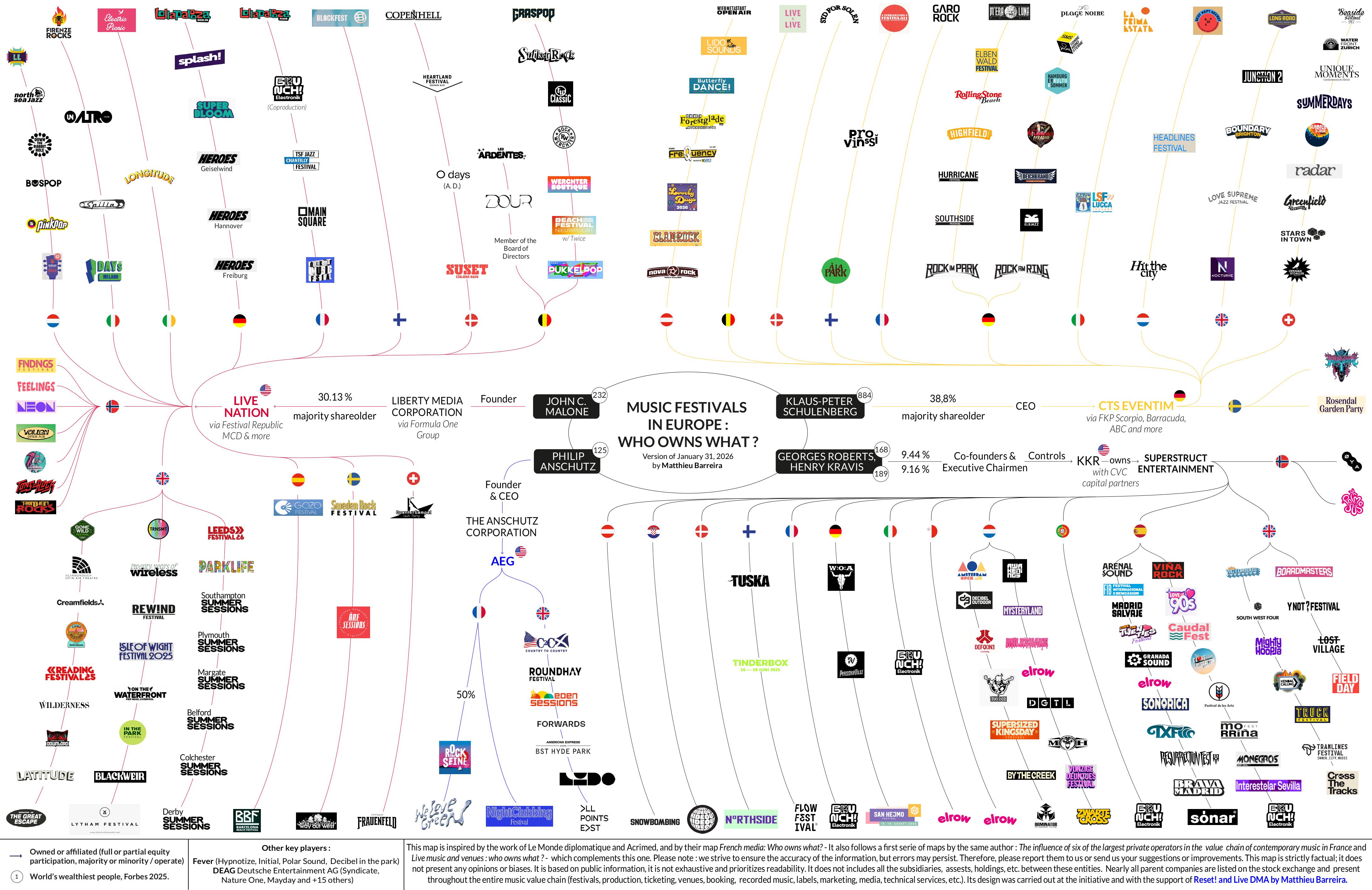

According to the latest mapping, more than 150 of the European Union’s largest music festivals are operated or controlled by just four international groups: Live Nation, Anschutz Entertainment Group (AEG), CTS Eventim, and Superstruct Entertainment.

Superstruct, which was acquired in 2024 by private equity firm KKR with CVC Capital Partners as co-investor, owns and operates more than 80 music festivals across ten countries in Europe and Australia. Its portfolio includes events such as Wacken Open Air, Tinderbox, Zwarte Cross, and Sónar.

Live Nation operates around 120 subsidiaries within the European Union and reported global revenue of approximately $16.7 billion in 2022.

AEG Presents, the live events division of Anschutz Entertainment Group, is widely described as the world’s second-largest live music promoter and combines concert promotion with ownership and operation of major venues, including London’s O2 Arena and Berlin’s Mercedes-Benz Arena.

CTS Eventim, one of the leading international providers of ticketing and live entertainment services, generated €1.9 billion in revenue across more than 20 countries in 2022 and operates ticketing platforms such as eventim.de, oeticket.com, and ticketone.it, alongside venue assets including Lanxess Arena in Cologne and the Waldbühne in Berlin.

By comparison, the 2,280 music venues and clubs represented in Live DMA’s network reported total income of €1.7 billion in 2019, corresponding to an average annual income of roughly €0.75 million per venue.

The updated ownership maps build on earlier editions that documented multinational investment in European festivals.

The new release integrates recent structural changes, including Superstruct’s acquisition by KKR and CVC, and shows continued expansion among the largest operators between 2022 and 2025.

During this period, the number of mapped festivals linked to Live Nation increased from 74 to 78, Superstruct from 34 to 63, CTS Eventim from 42 to 51, and AEG from 5 to 10.

Venue ownership shows a related but distinct pattern. The research indicates that consolidation efforts have primarily focused on arenas and stadiums rather than small and mid-sized venues.

Groups such as AEG, Live Nation, and CTS Eventim operate or hold stakes in some of Europe’s largest arenas and stadiums, often as part of broader real-estate or mixed-use developments. These venues are closely connected to the current boom in arena and stadium touring, which trade sources have described as the busiest period on record for global stadium activity.

Ticketing is identified as another central node in the live music value chain. Several of the major live music groups also control or operate large-scale ticketing platforms.

Live Nation’s ownership of Ticketmaster, frequently cited in policy and market analyses as the world’s largest ticketing company, is often referenced in discussions around speculative resale practices, access to high-demand events, and the broader impact of ticketing concentration on market diversity.

At the other end of the spectrum, most small and medium-sized music venues remain independent, associative, municipal, or locally owned, according to research from the European Parliamentary Research Service. These venues typically function as entry points for emerging artists and niche scenes and operate with limited margins under increasing pressure from real-estate costs, inflation, and regulatory requirements. They are commonly described as “incubators” for new talent, absorbing a significant share of artistic and financial risk in the early stages of artists’ careers.

Large corporate operators are also exposed to inflation, regulatory requirements, and changing audience behaviour. However, the mapping project highlights differences in how value circulates through the sector.

When artists progress from clubs to major festivals and stadium tours, the additional revenues generated at later stages generally do not flow back to the smaller venues that supported early career development. In most European countries, there are currently no structured mechanisms to redistribute value to the grassroots level.

Taken together, the ownership maps and related studies suggest that while consolidation may appear limited in numerical terms, a small number of transnational groups control a substantial share of high-capacity festivals and arenas and generate some of the highest revenues in the sector. When capacity, artist throughput, and revenue are considered, the research characterises the live music market as increasingly resembling an “oligopoly fringe.”

By making ownership structures more visible, the European Mapping Project aims to support informed discussion among policymakers, industry professionals, and the wider public about how Europe’s live music ecosystem is organised and how value is distributed across its different layers.

The report is published by Live DMA (Live Music Developing Artists) which is a pan-European network representing small and medium-sized live music venues, clubs, and festivals

Read the full report here

Find European Festivals here

With VIP-Booking.com, you can search for anyone in the live music industry - try it yourself!

Search Artists:

Trusted by professionals in the live music industry around the world for 25 years!